EUR/USD plunges as conflict and the ECB converge

The euro has been caught in the crosshairs of the Ukraine crisis as it absorbs the most selling of all major currencies since Russia’s invasion. The single currency has fallen five big figures since late February. The region is expected to take the biggest hit to economic activity, and this is set to delay the ECB’s plans to tighten monetary policy. Poorer growth prospects will also have to battle with ever higher inflation, as stagflation fears grow louder.

This is a toxic mix of stagnant growth and inflationary supply shocks.

European assets have been hammered in the last few weeks with Germany’s 10-year bond yield sinking into negative territory for the first time in a month. Stocks in the region have also tumbled with the continent’s Eurostoxx 50 index sliding by 15% and Germany’s flagship Dax index entering a bear market this week, having fallen more than 20% from recent highs. The sell-off of the past two weeks means European equities are now 25% cheaper than the rest of the world on a forward price-to-earnings basis, the biggest discount since the eurozone debt crisis in 2011.

Economists are starting to forecast a potential technical recession in the zone.

That means two consecutive quarters of negative GDP growth, which several estimate could start at the beginning of 2023. With a war on their doorstep, will consumers go out and spend their savings they’ve built up through the pandemic? That’s even before you consider the huge jump in inflation.

ECB to hold off on any policy decisions

Relative to the Fed especially, the Ukraine crisis leaves the ECB who meet on Thursday in a tough spot, given the trade, inflation and humanitarian impact. Lower growth will disrupt trade and confidence of households and businesses. Upgraded inflation forecasts close to its target of two per cent over the next two years will be slightly meaningless as that means the bank should be tightening policy and raising rates.

But recent comments from ECB officials have cautioned against repeating past mistakes of tightening policy too early, especially in the face of the supply shock caused by the Ukrainian crisis.

A light touch by President Lagarde is seen as the way forward, taking careful step as the fallout from the geopolitical events unfolds. This marks a shift in tone from just a few weeks ago when a normalisation of policy and an interest rate rise by the end of the year was forecast.

Euro downside risks remain

The recent performance in EUR/USD has been warranted by the divergence in European and US assets, as well as central bank expectations. The S&P500 is relatively “outperforming”, down roughly seven per cent, while the Fed is still expected to go ahead with a quarter point rate hike next week. This will probably be bolstered by the US CPI data also released on Thursday, which is forecast to print near 8% versus 7.5% in January.

Technically, the major is oversold on several indicators with the daily RSI at levels last seen in February 2020. EUR is finding a small bid this morning on news that the EU is mulling a large joint bond sale to fund energy and defence.

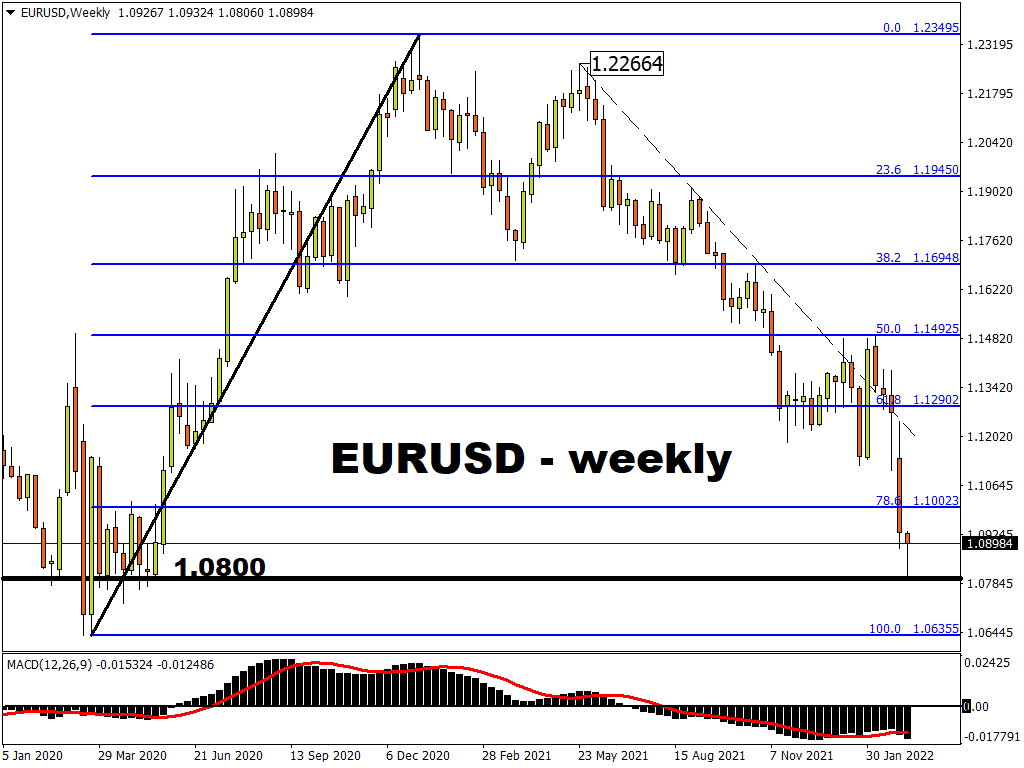

The key break of the 1.11 support zone saw prices quickly plummet to near two-year lows and into longer-term support around the February/March 2020 trough. Near-term resistance is 1.09 followed by the mid-figure area and then 1.10. Losses may decelerate for a time here as technical conditions ease, but sellers will keep their focus on the 2020 low at 1.06355 if there is no end in sight to the conflict.