Evergrande story creeps back into markets

European markets have opened up modestly lower on the back of softness seen in Asia overnight. The upbeat mood from the near-record highs hit in US indices on Wednesday has been replaced by fresh worries over the weakening Chinese property sector as a possible default by China Evergrande looms.

This could come as soon as next Saturday after a proposed $2.6billion deal collapsed sending Evergrande shares into a double-digit decline. However, this may force Beijing to act more swiftly in supporting the broader credit markets. Ultimately, we may be closer to “peak stress” for now.

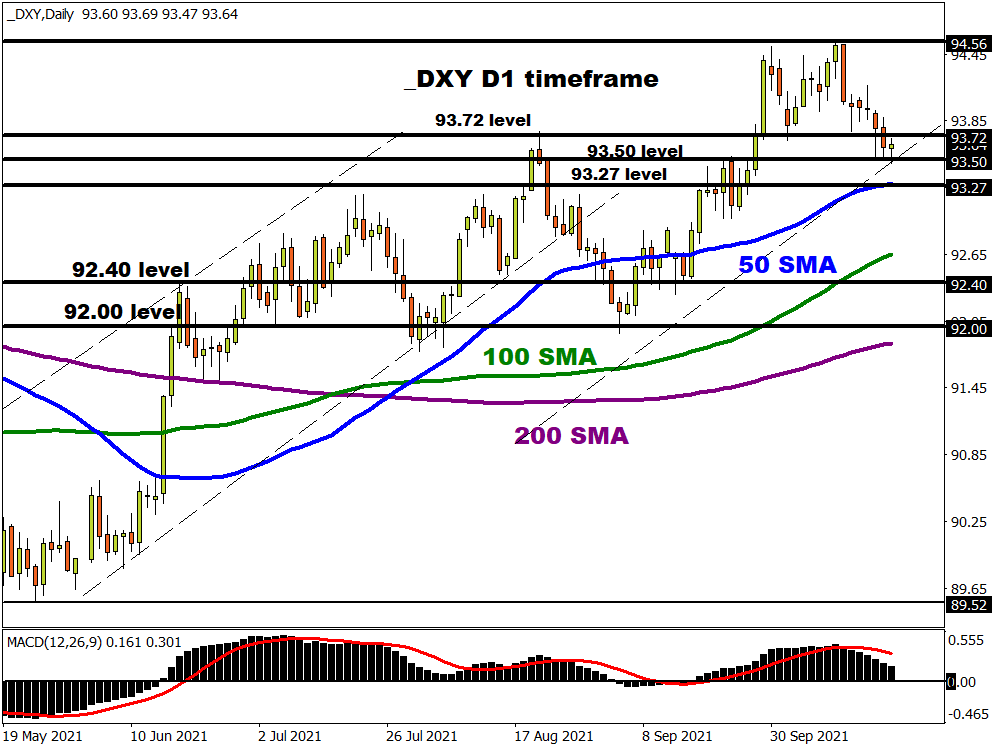

Dollar weakness ongoing

The greenback remains on the defensive after printing multi-month highs on the DXY last week. Overnight, US Treasury yields hit levels not seen since May with a high at 1.67% and this has helped the dollar stabilise above 93.50. The DXY is heavily weighted to European FX and should find some support above 93 and the 50-day moving average at 93.27.

Europe is not well positioned in the global energy crisis with both energy and supply chain disruptions hindering the recovery. The ECB’s cautious stance towards any kind of policy normalisation remains a feature as well, with news that German Bundesbank President Weidmann will resign at the end of the year not helping the hawks’ cause on the Governing Council.

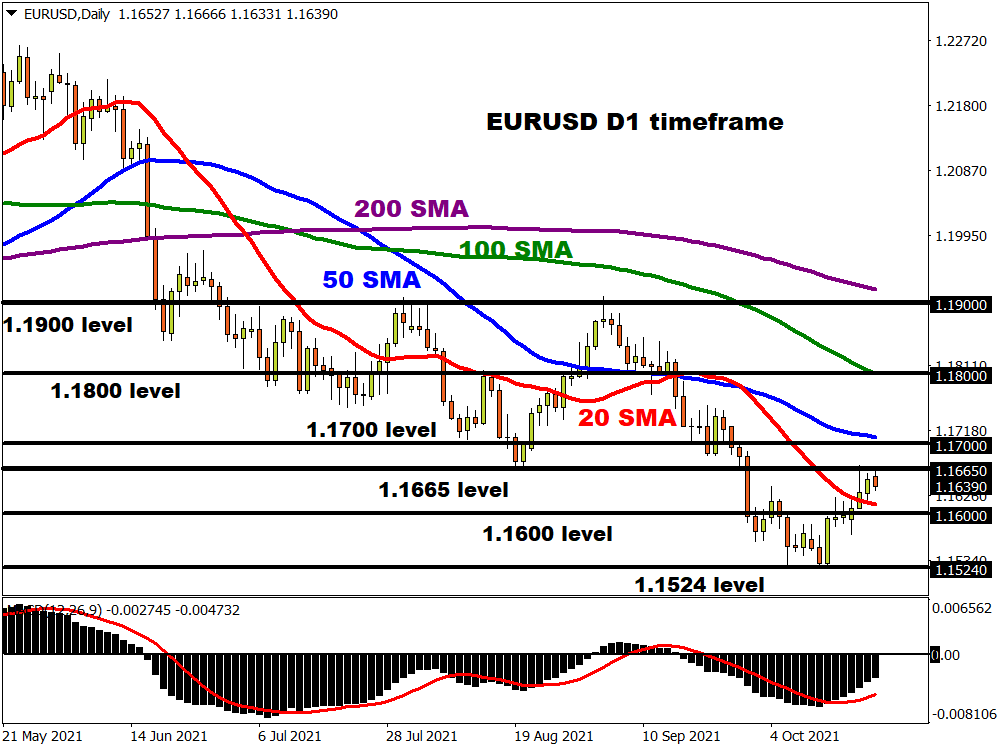

The recent euro rally has halted at a key short-term resistance level around the August low at 1.1665 in EUR/USD. A minor bull channel is still intact, though the daily RSI has paused at 50 which could mean a period of sideways trading. A break below the recent range at 1.16 would point to a renewed push south towards the October low at 1.1524. A meaningful move through 1.1665 will see the world’s most traded currency pair trade into trendline resistance from the June highs above 1.17.

Oil hovering near highs

The oil market pushed higher again yesterday after a constructive inventory report from the EIA. Crude oil inventories at Cushing fell, leaving them at their lowest levels since 2018. Oil strategists say if this trend continues, there will be growing concerns over hitting tank bottoms.

Persistent strength in prices also means pressure on OEPC+ to increase output is growing. The US and India have already asked the cartel to pump more, but the group is wary of additional non-OPEC+ supply growth next year. The next OPEC+ meeting is scheduled for November 4.

Bulls have the October 2018 high at $86.71 firmly in their sights with the June 2012 spike low at $88.52 the next long-term marker. Initial support sits at $83.66/73.