Week Ahead: Stocks, dollar await NFP catalyst

It’s been a quiet week for US stocks, with the VIX index (Wall Street’s “fear” gauge) falling to its lowest levels since April. At the time of writing, the futures contracts for all 3 major benchmark indices are in the green, with the S&P 500 set to end a run of two consecutive weekly declines. The blue-chip index could well add to its 1.08% week-to-date gains ahead of the long Memorial Day weekend.

With less than one percent separating the S&P 500’s current price and its highest-ever closing price, we shall see whether this index can post a new record high over the coming week:

Monday, May 31

- US, UK markets closed

- China manufacturing/non-manufacturing/composite PMIs

- Japan industrial production, retail sales, consumer confidence

- OECD economic outlook

Tuesday, June 1

- Manufacturing PMI: China, Eurozone, UK, US

- RBA policy decision

- BOE Governor Andrew Bailey speech

- Fed speak: Fed Governor Lael Brainard

- OPEC+ meeting

Wednesday, June 2

- Fed speak: Philadelphia Fed President Patrick Harker, Chicago Fed President Charles Evans, Atlanta Fed President Raphael Bostic, Dallas Fed President Robert Kaplan

Thursday, June 3

- Services/composite PMIs: China, Eurozone, UK, US

- US initial jobless claims

- EIA crude oil inventories

Friday, June 4

- Panel discussion with central bank heads: Fed Chair Jerome Powell, ECB President Christine Lagarde, PBOC Governor Yi Gang

- Eurozone retail sales

- US nonfarm payrolls

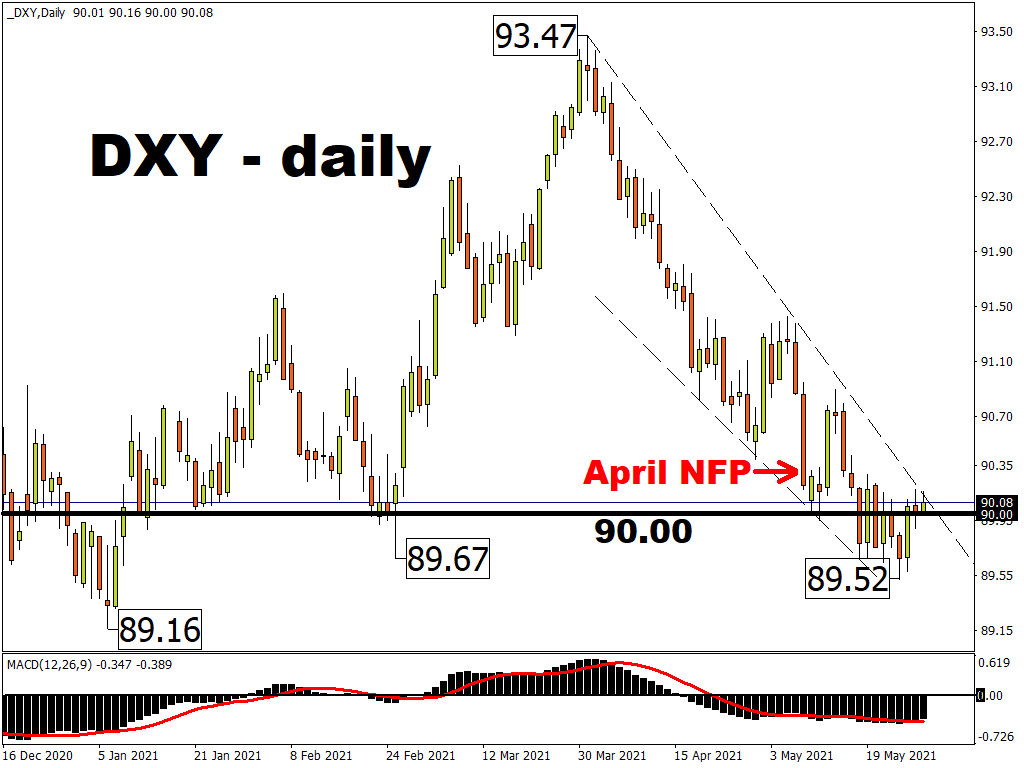

The May US nonfarm payrolls release is set to dominate market chatter this week. Recall that the April print was abysmally low, coming in at a measly 266,000 vs. the one million figure expected.

For the May print, markets are forecasting that 663,000 jobs were added in the US this month.

Another lower-than-expected print could translate into a bigger pullback in expectations that the Fed might taper its asset purchases sooner-than-expected. This would be down to policymakers’ unwillingness to unwind its support before the US jobs market is on a firmer footing.

Such a narrative could lead to suppressed US Treasury yields, which could then lead to downward pressures for the dollar index (DXY).

Recall that the 7 May release of the April NFP triggered a 0.8% decline in the DXY, which was its biggest single-day decline since November, shortly after the US presidential elections.

While economists have since tried to readjust their expectations for the US labour market, dollar bulls could ill afford another negative surprise. Such an event risks a new year-to-date low for the greenback.