Week Ahead: US jobs report, OPEC+ decision ensure active start to 2022

Once the dazzling fireworks and the renditions of Auld Lang Syne have faded away, global investors will be back to the grind in the first week of 2022.

Familiar themes will continue to dominate market sentiment in the new year, such as the global inflation outlook and the response by major central banks, and will be used to interpret the coming week’s economic calendar:

Monday, January 3

- EUR: Eurozone December Markit manufacturing PMI (final)

- USD: US December Markit manufacturing PMI (final)

Tuesday, January 4

- CNH: China December Caixin manufacturing PMI

- Brent: OPEC+ meeting

- USD: US December ISM manufacturing

Wednesday, January 5

- EUR: Eurozone December services and composite PMIs (final)

- US crude: EIA weekly US crude oil inventory report

- USD: FOMC minutes

Thursday, January 6

- CNH: China December Caixin services and composite PMI

- EUR: Germany December CPI and Eurozone November PPI

- USD: Fed speak – St. Louis Fed President James Bullard, US weekly jobless claims

Friday, January 7

- EUR: Germany November industrial production and Eurozone December CPI

- USD: US December nonfarm payrolls

- USD: Fed speak – Atlanta Fed President Raphael Bostic, San Francisco Fed President Mary Daly, Richmond Fed President Thomas Barkin

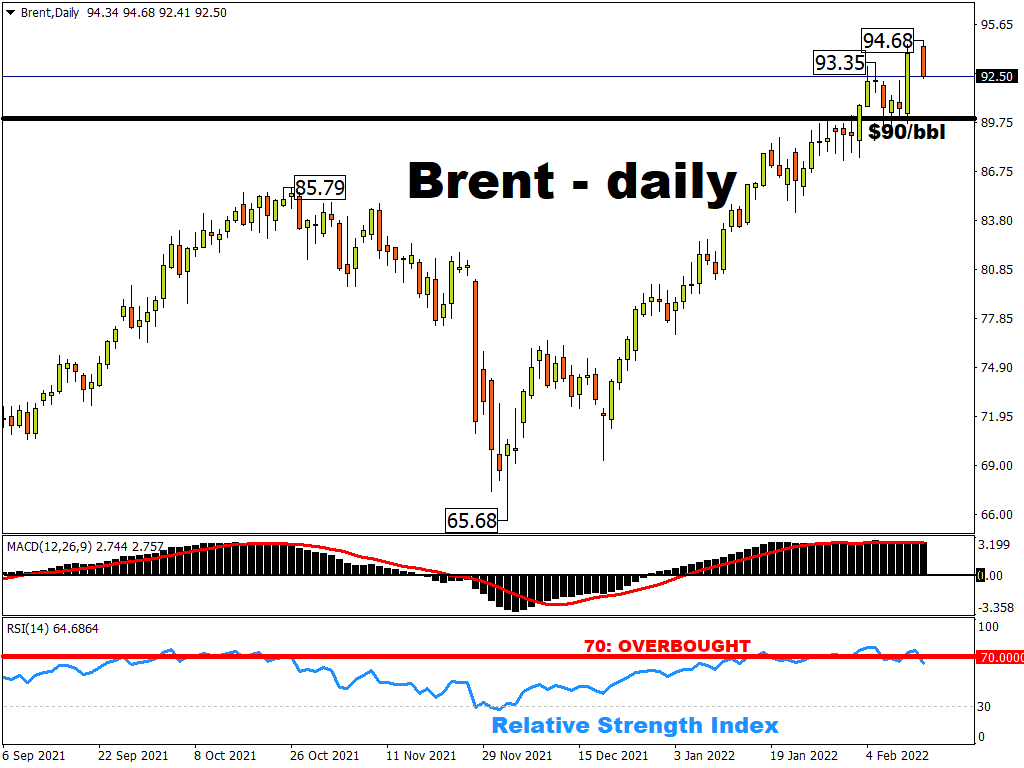

OPEC+ set to stick with gradual output hikes

Oil prices have had a remarkable 2021. Brent futures are on course for an annual gain of over 53% while WTI futures should boast of an annual advance of 58%; which would respectively be their best yearly performance since 2009.

OPEC+ is due to make another decision about whether to press ahead with an additional 400k barrels per day (bpd) in restored output. While recent reports have shown that Omicron’s impact on global demand has been milder than expected thus far, it remains to be seen how the alliance will take into account such unknowns.

A decision next week to raise OPEC+ production by another 400k bpd in February shouldn’t rock markets.

The bigger OPEC+ surprise would be to pause its gradual output restoration, which had been the market’s expectation for the December meeting.

Such a scenario could help Brent resurface above $80/bbl and keep prices above that psychologically-important level for the immediate term.

US jobs report to hold court for FX markets

Besides any fresh clues from the FOMC meeting minutes due mid-week, FX markets will also be honing in on the December US nonfarm payrolls report due Friday. Current estimates call for a headline print of about 400,000, and for the unemployment rate to improve by another 10 basis points down to 4.1%.

Although the jobs recovery has now ceded to inflation pressures as being the Fed’s primary consideration for its next policy steps, the NFP remains a key factor for global markets. Signs that the US labour market is mending further, despite Omicron’s threat, should support the notion that inflation in the world’s largest economy could see more demand-pull forces. And this is where wage growth plays a crucial factor from this Friday’s data.

A robust US jobs report that shows better-than-expected wage growth and total jobs added could lower the bar for the expected Fed rate hike.

Such a notion should help the benchmark US dollar index (DXY) break to the upside from its current range, and build on 2021’s annual advance of about 6.8% which is its best year since 2015.