OPEC+ meeting in focus as oil markets look for some support

European markets are in the red this morning with the dollar holding its ground, while US futures remain in positive territory at the time of writing. Yesterday was another rollercoaster session with intraday volatility in full effect. Stocks looked like they were heading for a healthy rebound when news of the first case of Omicron being found in the US saw sharp risk-off sentiment engulf markets.

Most sectors sold off with the Nasdaq faring the worst, tumbling 1.8% as reopening plays and growth and momentum stocks got hit. The Vix shot up, closing north of 30 which is the highest implied volatility since January.

Cartel to decide on planned January output hike

It’s a key day for oil markets and commodity currencies as OPEC+ make a decision on whether to go ahead with their already agreed 400k barrels per day output increase in January. Markets appear widely positioned for a delay in the hike given the huge uncertainty related to the Omicron variant and any subsequent hit to demand.

The option of more cuts is apparently not off the table and this type of action would be in line with the cautious approach adopted by the cartel since the beginning of the pandemic. Some analysts are also citing previous instances of the Saudi energy minister surprising markets over the last 18 months.

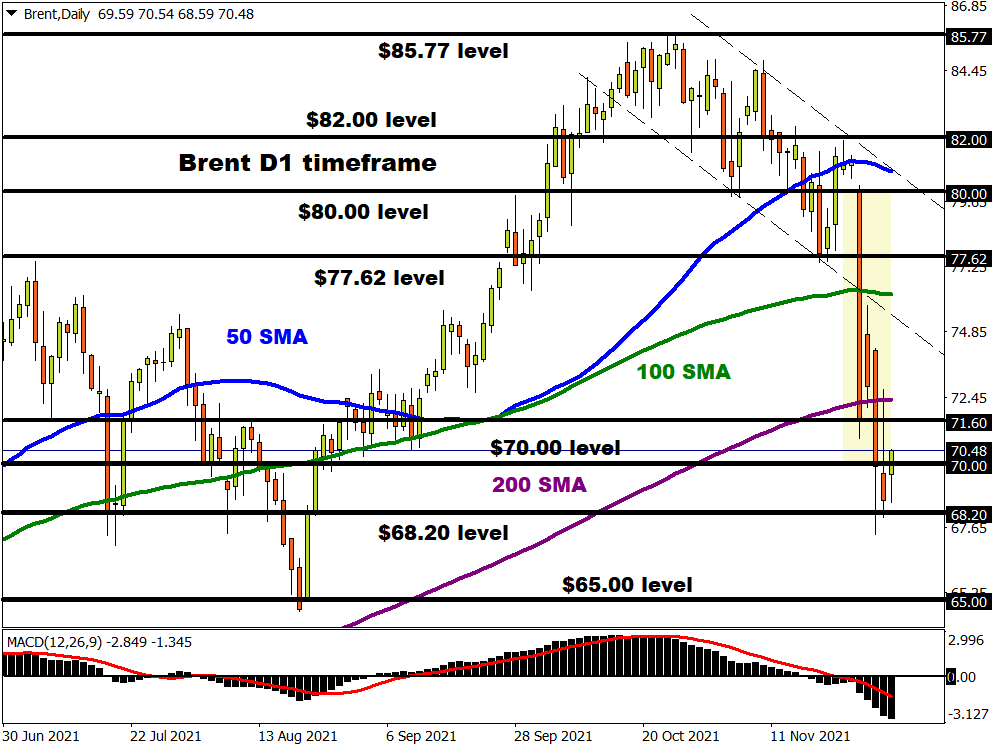

Brent is currently trading above $70 which leaves it roughly less than 20% below the recent high seen in late October at $86.68. Prices are comfortably beneath the 200-day simple moving average at $72.30 and long-term trendline support/resistance from the 2020 pandemic lows.

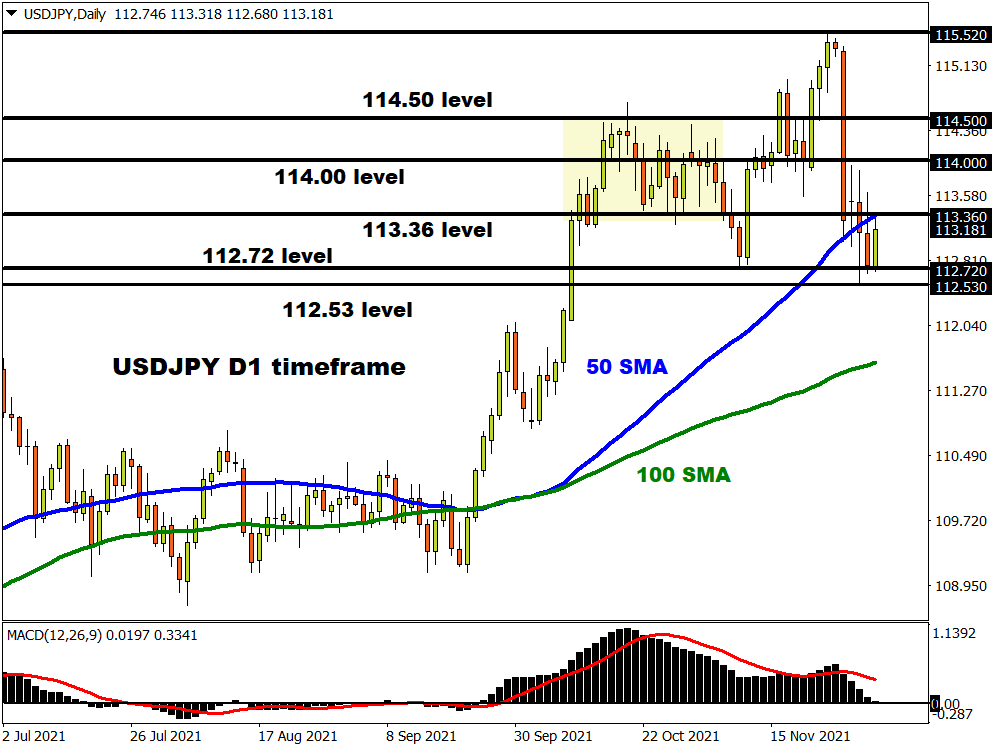

USD/JPY holding onto support

The tone in FX continues to be largely set by moves in equities and the overall risk mood. US bond yields are picking up this morning after Fed Chair Powell said the Fed needs to be ready to respond to the possibility that inflation may not recede in the second half of next year as most forecasters currently expect. This would likely lead to an acceleration in the pace at which the Fed tapers its asset programme.

We get jobs data today and tomorrow in the US. Weekly jobless claims figures released this afternoon will be watched after last Thursday’s drop below 200,000. Another strong print will add further pressure to policymakers with Friday’s non-farm payrolls forecast for a solid print above 500k. Given the material downside risks caused by the Omicron variant, markets will need strong data to avert renewed dovish pricing.

Friday’s plunge in USD/JPY took us from the highs at 115.52 back into the previous couple of months range. The major printed a new pivot low at 112.53 on Tuesday and we are now consolidating around 113. The 50-day moving average sits above at 113.36 while initial support on the downside comes in at the November lows at 112.72. US bond yields will have much to say about where USD/JPY heads in the near term with 1.40% now a key level in the 10-year Treasury.