Week Ahead: GBPUSD caught in ‘battle of the hawks’

Inflation, inflation everywhere. And more rate hikes are coming!

That’s been the refrain across global financial markets in recent months, and will continue guiding the attention of investors and traders in the coming week:

Monday, February 14

- EUR: ECB President Christine Lagarde speech

- S&P 500: 13F filings

Tuesday, February 15

- JPY: Japan 4Q GDP, December industrial production

- GBP: UK December unemployment, January jobless claims

- EUR: Eurozone 4Q GDP, Germany February ZEW survey expectations

Wednesday, February 16

- CNH: China January CPI and PI

- GBP: UK January CPI and PPI

- EUR: Eurozone December industrial production

- US crude: EIA crude oil inventory report

- CAD: Canada January CPI

- USD: FOMC minutes, January retail sales and industrial production

Thursday, February 17

- AUD: Australia January unemployment

- JPY: Japan January external trade

- EUR: ECB publishes economic bulletin, ECB Chief Economist Philip Lane speech

- USD: US weekly jobless claims

- USD: Fed speak – Cleveland Fed President Loretta Mester, St. Louis Fed President James Bullard

Friday, February 18

- GBP: UK January retail sales

- EUR: Eurozone February consumer confidence

- USD: Fed speak – Fed Governor Lael Brainard, Chicago Fed President Charles Evans

The UK’s January consumer price index will be scrutinized for signs whether the Bank of England will have its work cut out for it in its battle against inflation. Having registered a 5.4% year-on-year print in December, its highest since 1992, the headline CPI figure is forecasted to tick higher to 5.5% in January.

While noting the lag before seeing the effects of monetary policy changes, markets are well aware of the back-to-back hikes already initiated by the BOE so far (15 basis point hike in December, and another 25 basis points in February). On top of that, four of the nine members of the Monetary Policy Committee voted for a 50-basis point hike at this month’s meeting – something never before seen out of the BOE since it gained independence in 1997.

The UK GDP figures just released today, which showed that the economy grew at its fastest pace since World War 2, could have paved the way for that 50-bp hike to be triggered at the next BOE meeting. The GDP prints are likely to have assuaged policymakers over concerns whether the economy can handle such an unprecedented policy move.

As things stand, judging by the overnight index swaps, markets are already anticipating a 50-basis point hike in March, as the BOE front loads its policy firepower in a bid to quell inflation.

The bank rate is forecasted to rise from the current 0.5% to hit 2% by November – that’s a lot of rate hikes being baked in.

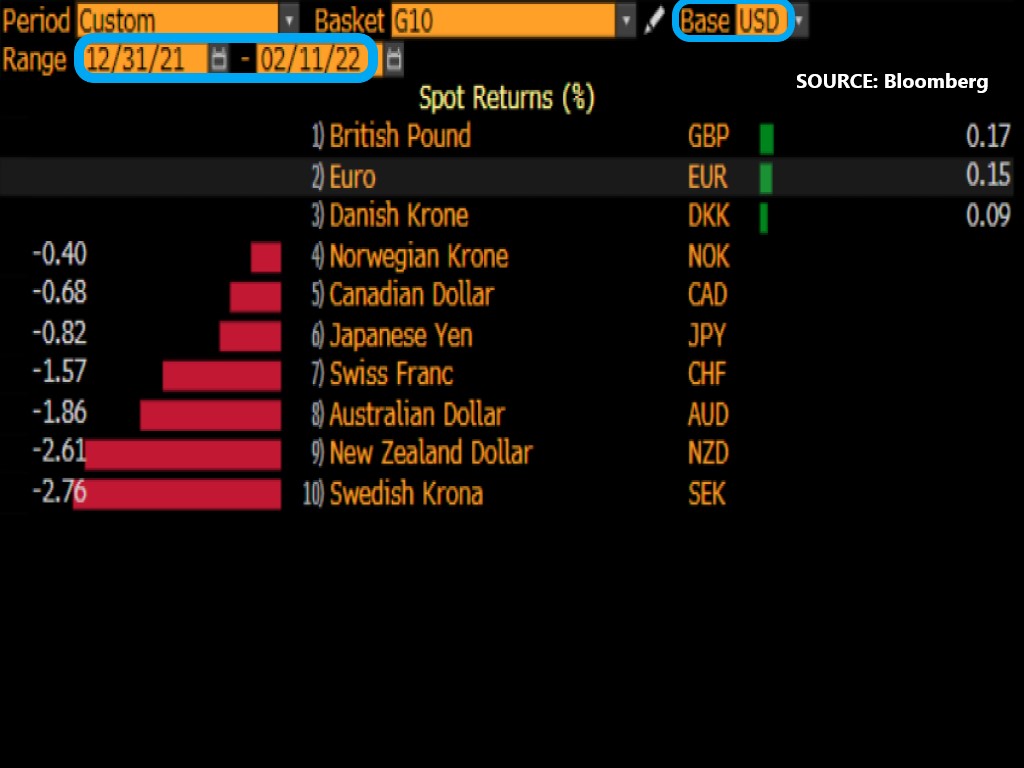

Such hawkish expectations have already propelled Sterling into being the best-performing G10 currency against the US dollar so far this year.

If next week’s inflation print gives extra ammo to the MPC hawks, and markets shift their expectations accordingly, that could entice Pound bulls into sending GBPUSD on its way to test its 200-day simple moving average as a resistance level.

Whether or not ‘cable’ can hold onto gains in the aftermath of a potentially higher-than-expected UK CPI print would of course depend on what happens on the other side of the pond.

The US dollar will remain sensitive to clues about the Fed’s next move, even as markets continue to debate the size of the looming Fed rate hike next month.

For immediate consideration, the latest FOMC minutes are due for a mid-week release, followed by several episodes of Fed speak before next weekend.

Further signs that the Fed must also come out guns blazing in this policy tightening cycle could spur the buck into advancing further, potentially dragging GBPUSD below its 100-SMA.

This scenario also assumes that the UK inflation prints come in lower-than-expected, with signs of plateauing inflationary pressures then easing off the pressure on the BOE to adopt such an aggressive stance.