Week Ahead: Inflation obsession to drive dollar and gold

The Fed policy outlook is all the rage across global financial markets.

Hence, Thursday’s US consumer price index release is set to grab the spotlight in the coming week, amidst these scheduled economic data events and US earnings announcements:

Monday, February 7

- China markets reopen after Lunar New Year

- CNH: China January Caixin services and composite PMIs

- EUR: Germany December industrial production

Tuesday, February 8

- JPY: Japan December trade balance and household spending

- USD: US December trade balance

Wednesday, February 9

- EUR: Germany December external trade

- GBP: BOE Chief Economist Huw Pill speech

- US crude: EIA crude oil inventory report

- USD: Cleveland Fed President Loretta Mester speech

- Disney earnings

- Uber earnings

Thursday, February 10

- EUR: European Commission’s updated economic forecasts

- GBP: BOE Governor Andrew Bailey speech

- USD: US January consumer price index

- Twitter earnings

- Coca-Cola earnings

- PepsiCo earnings

Friday, February 11

- GBP: UK 4Q GDP and external trade, December industrial production

- EUR: Germany January consumer price index

- USD: US February consumer sentiment

Last month, inflation in the world’s largest economy is forecasted to have risen by 7.3%. If confirmed, that would be the fastest surge in consumer prices since February 1982.

Given that the Fed’s most-pressing goal now is to quell these inflationary surges, further signs of consumer prices rising unabated could well prompt policymakers into bringing out the big guns for the March FOMC meeting: a 50 basis-point hike.

If markets grow more expectant that a larger-than-usual Fed rate hike is in store, that could trigger another selloff in US Treasuries, pushing the dollar higher on the wings of rising yields. However, dollar gains may be tougher to come by, given the ECB’s hawkish pivot this week (note that the euro accounts for 57.6% of DXY).

But first, dollar traders must digest today’s US nonfarm payrolls report, with markets expecting a mere 125,000 jobs added in January. A lower-than-expected jobs report may not be enough to assuage investors who are increasingly expecting a more aggressive Fed, although some knee-jerk declines could play out in the benchmark dollar index (DXY).

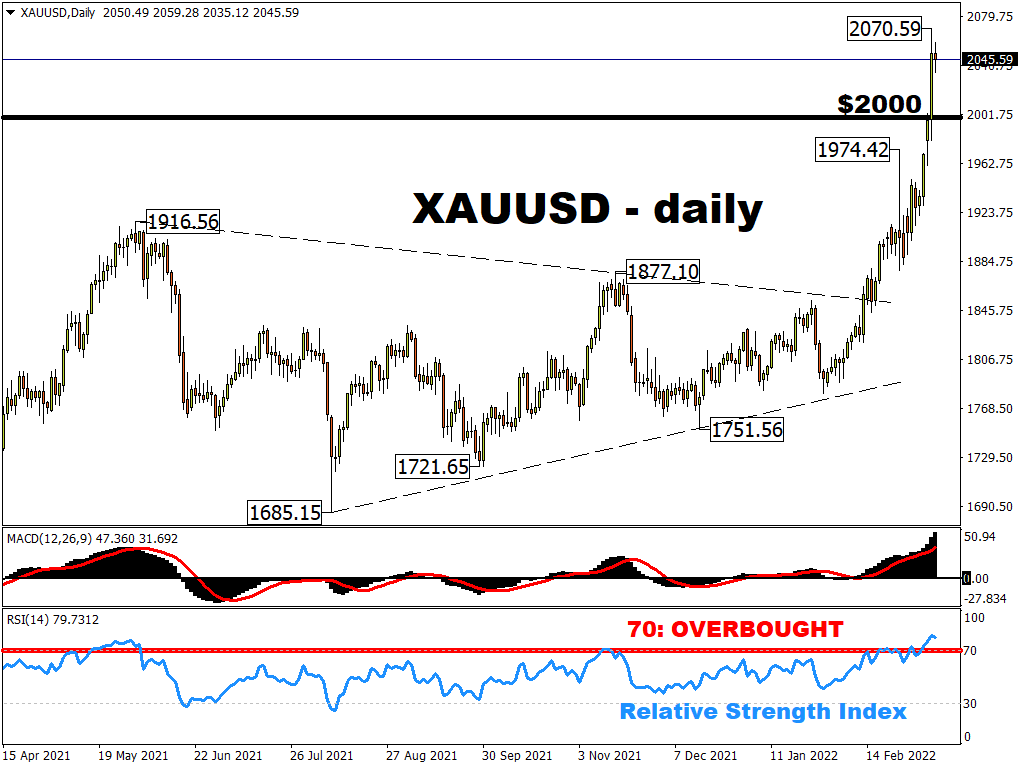

Gold could move lower on rising dollar/real yields

The greenback’s inverse relationship with gold should continue playing out, post-NFP and beyond. The precious metal is likely to remain rangebound for the time being, with bullion bugs reluctant to push prices higher, wary of another spike up in US Treasury yields.

Should nominal 10-year yields climb another leg higher closer towards the psychologically-important 2% mark, pulling real yields closer to positive territory, that should exert more downward pressure on spot gold despite its traditional role as an inflation hedge.

Still, the precious metal could see some measure of support from persistent fears over geopolitical tensions as well as the seasonal demand from the Lunar New Year. However, the latter is set to wane soon, leaving the precious metal even more exposed to gyrations in the buck and real yields.